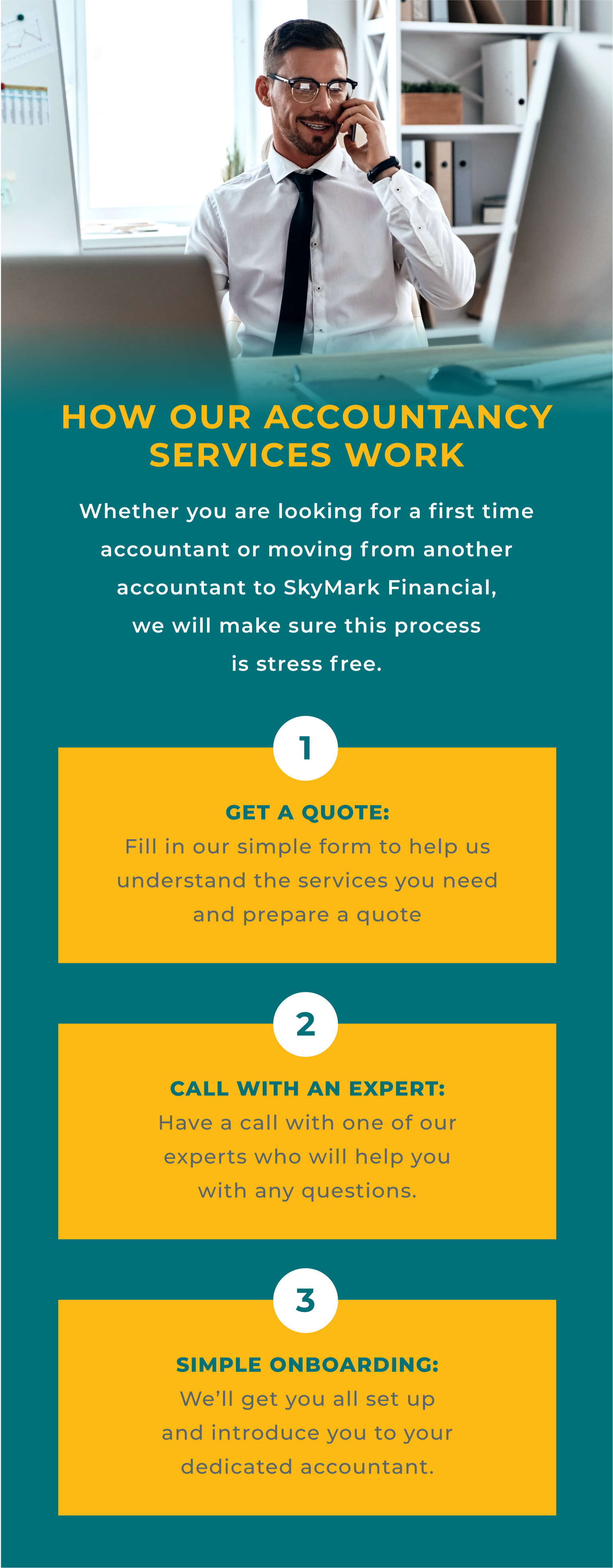

At Skymark Financial we are experts in providing accountancy services for small to medium sized businesses with over 40 years experience with SMEs, this is why we understand that not one size fits all when it comes to accountancy needs.

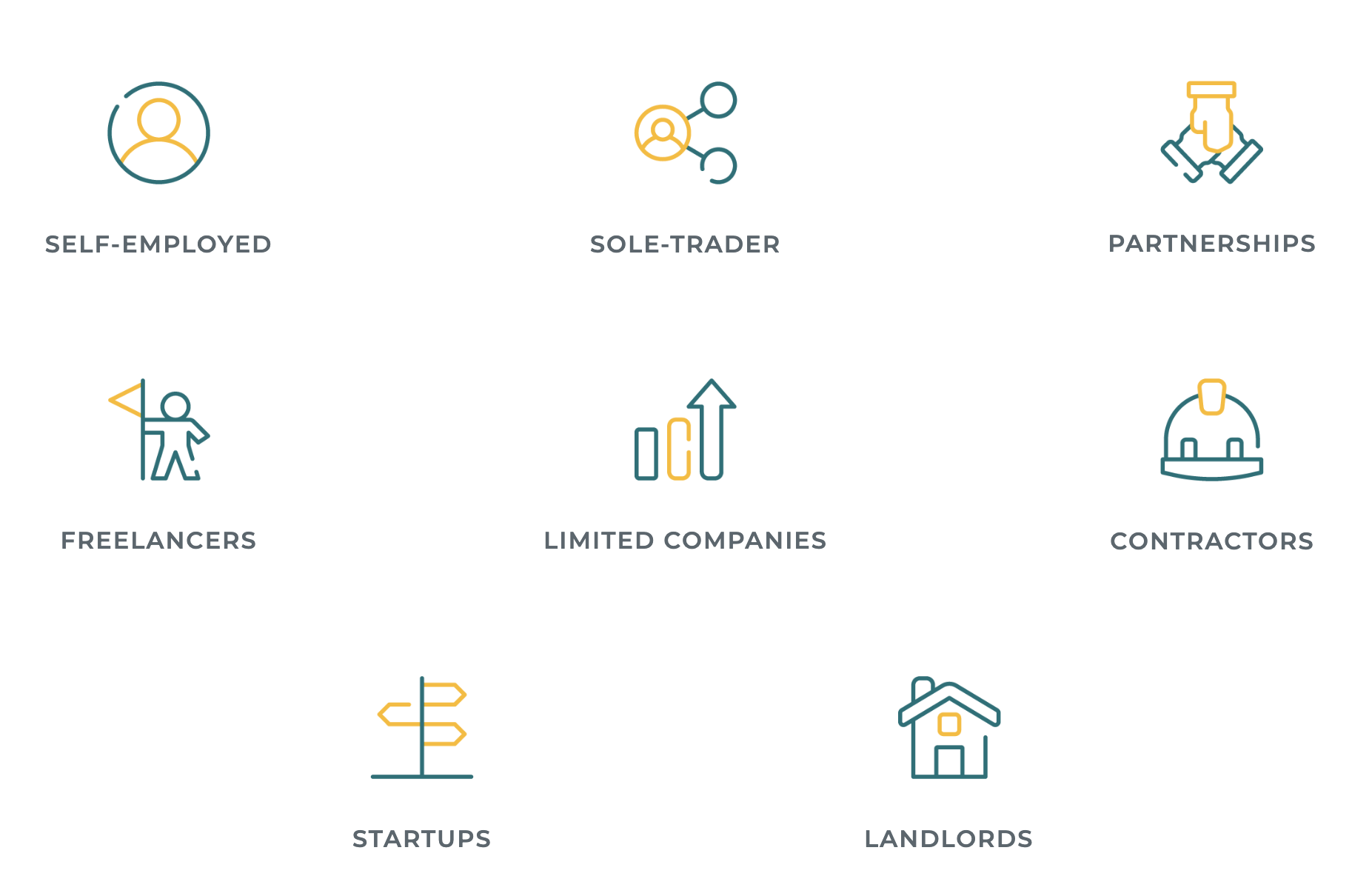

WHO WE HELP

With over 40 years in the industry we have supported businesses of all shapes and sizes, so let us take care of your accountancy needs while you focus on your passion which is your business.

SELF-EMPLOYED

SOLE-TRADER

PARTNERSHIPS

FREELANCERS

LIMITED COMPANIES

CONTRACTORS

STARTUPS

LANDLORDS

WHO WE HELP

With over 40 years in the industry we have supported businesses of all shapes and sizes, so let us take care of your accountancy needs while you focus on your passion which is your business.

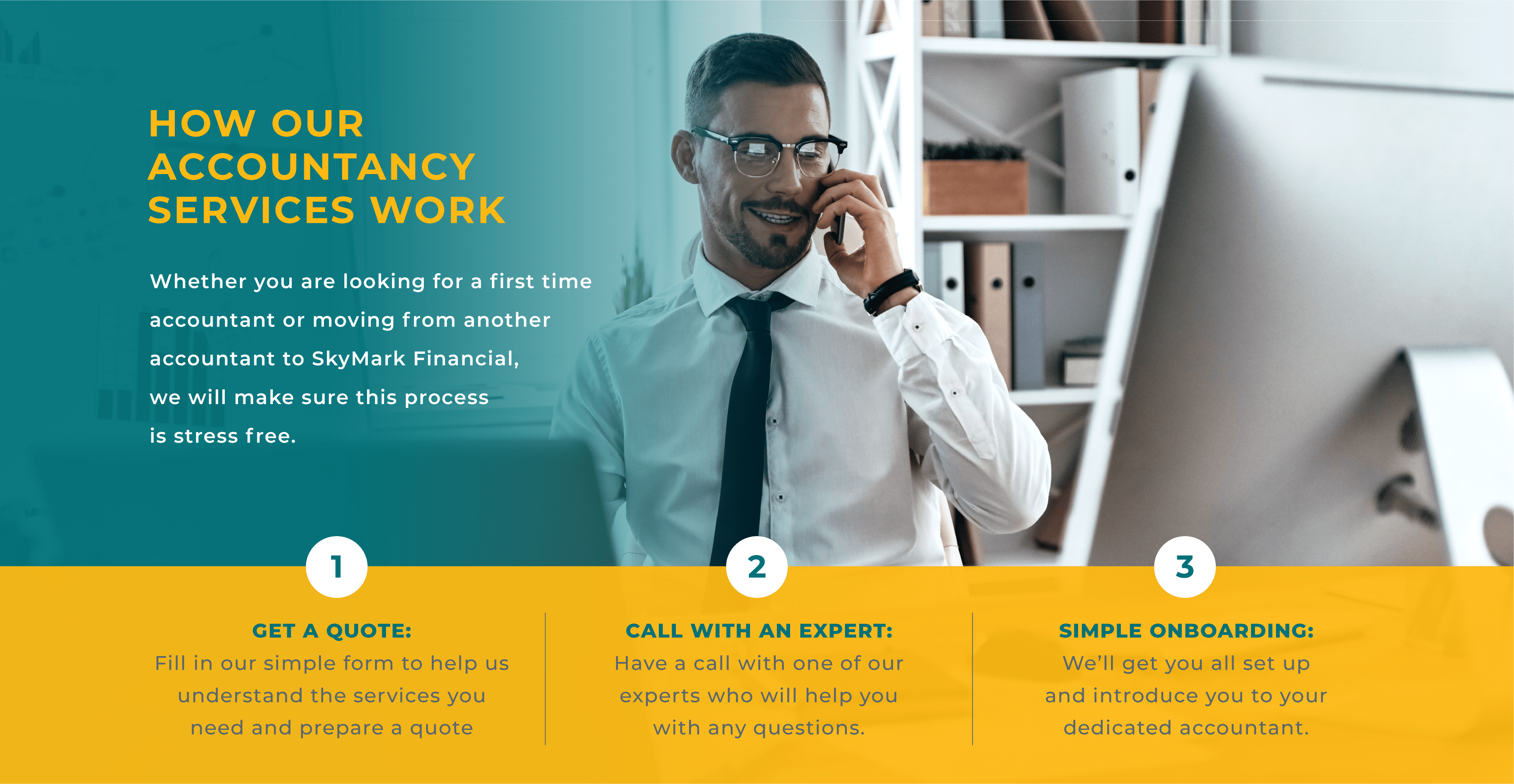

WHY CHOOSE US FOR YOUR BUSINESS ACCOUNTANCY NEEDS

WHY CHOOSE US FOR YOUR BUSINESS ACCOUNTANCY NEEDS

YOUR OWN DEDICATED LIMITED COMPANY ACCOUNTANT

When you join us, you will receive your very own dedicated limited company accountants. Our fully qualified and friendly team will be on hand to help you throughout the year for all your financial queries.

SIMPLE

ACCOUNTING

SOFTWARE

You are provided with leading accounting software from one of our partners which will help reduce the time it takes to keep on top of your accounting records and bookkeeping.

UNLIMITED

EXPERT

ADVICE

Our dedicated accountants possess extensive accounting knowledge and can easily handle simple and complex processes, including tax return filing, accounts preparation, company formation, VAT returns management, etc.

BESPOKE SERVICE OPTIONS TO SUIT

YOUR BUSINESS

We offer full service packages which you can choose from depending on the size of your business, however we understand that each business is different and may require a bespoke set of services.

TAX

EFFICIENCY

REVIEWS

Your dedicated accountant will conduct annual tax efficiency reviews to make sure your business is operating in the most tax efficient way, claiming for every possible expense.

WHAT OUR CLIENTS SAY

WHAT OUR CLIENTS SAY